Why Does Venmo Make Payments Public?

How social payments replaced institutional trust with visibility.

Open Venmo and scroll the feed. It feels like you’ve picked up someone else’s itemized diary: rent splits, taco reimbursements, the occasional passive-aggressive 🙃. The dollar amounts are hidden, but the relationships are not.

The instinctive reaction is simple: why is any of this public?

Venmo’s says payments are “fun to share.” The more interesting answer is institutional.

Money Used To Mind Its Business

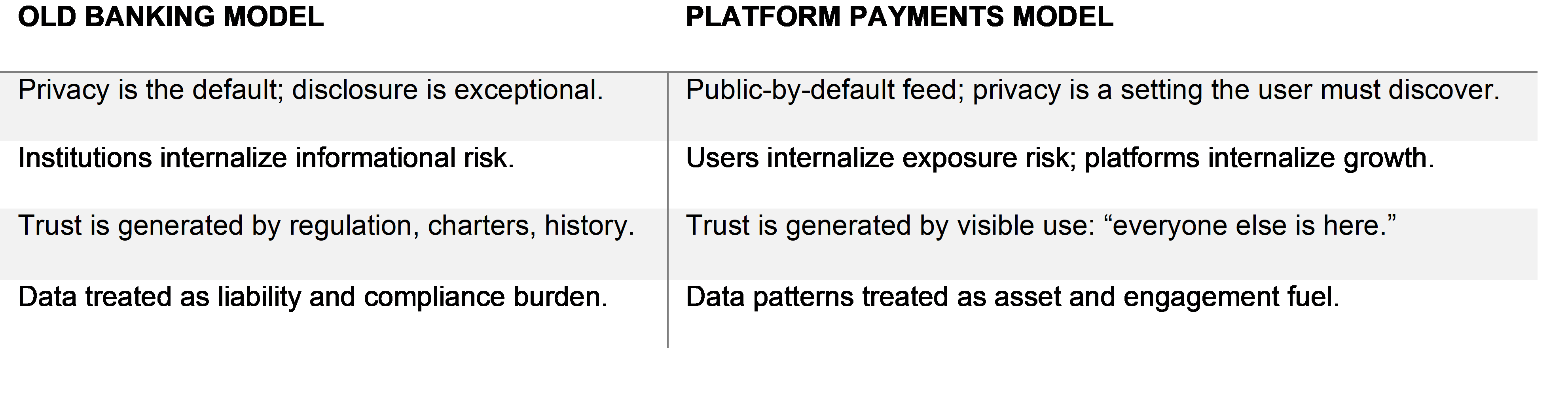

For most of modern banking, transactions were not supposed to become anyone’s content stream. Privacy wasn’t a boutique preference; it was part of the architecture. Banks sat between you and the world, clearing payments and absorbing the informational risk that came with knowing who paid whom.

That arrangement wasn’t sentimental. It was functional. Markets depend on the ability to transact without turning relationships and crises into public signals. Settlement stayed settlement because confidentiality lowered the social cost of exchange.

Venmo’s Problem: No One Trusts the Empty Room

Venmo was born without any of that inherited trust. No charter. No marble lobby. Just a scrappy app that only worked if enough of your friends were willing to route money through a social network owned by PayPal.

That’s a coordination problem, not a UX problem. A payment app is useless if the people you transact with don’t use it. Early on, any given person has almost no information:

· Will my friends actually adopt this?

· Is there real activity here, or am I walking into a ghost town?

· Will this thing still be around in two years?

Venmo’s problem wasn’t moving money. It was manufacturing confidence.

Traditional finance solves that with regulation, deposit insurance, and longevity as a repeated signal of reliability. Venmo had none of that. It needed another way to manufacture confidence.

So it reached for something platforms understand better than banks: visibility.

Visibility as a Substitute for Trust

Venmo’s public feed took what used to be a private confirmation — “the payment went through” — and turned it into a social signal: “look, people like you are using this all the time.”

· Each public payment is a little proof-of-life for the network.

· Each scrolling session is free marketing.

· Each “oh, she’s on Venmo too” interaction lowers adoption friction.

Venmo describes itself as a social network; people open the app to see what others are up to. Beneath that framing is an institutional shift: reputation is replaced by observable participation.

The innovation wasn’t faster money. It was visible money.

Defaults as Quiet Governance

Venmo emphasizes that users can adjust their privacy settings. Formally, that’s true. Economically, the power lies in the default.

Public-by-default means doing nothing produces visibility. Changing that requires attention, navigation, and effort. Behavioral economics has been clear for years: most people accept the default.

The older banking model embedded privacy in the structure itself. The platform model hands users a toggle and lets path dependence do the rest.

That shift — from “we’ll protect this” to “we’ll label the toggle” — is a small but telling change in how governance operates.

The Institutional Trade: Who Carries the Privacy Risk?

Once you see the trust problem, the rest of the design choice comes into focus. Venmo flips the old allocation of responsibility:

In the banking model, you don’t need to curate your financial exposure. The default architecture does it for you. In the platform model, the app hands you the controls — then quietly sets them to “broadcast,” and lets path dependence do the rest.

The FTC’s complaint against Venmo in 2018 was telling: regulators didn’t say “you can’t have a social feed,” they said you misled users about what was visible and buried key information behind confusing settings. The settlement forced better disclosures, not a return to privacy-by-default.

That is the institutional pivot in miniature: from “we’ll protect this” to “we’ll label the toggle.”

The Externalities Are Boringly Predictable

None of this requires a sinister plot, and you don’t need to invoke “surveillance capitalism” to see the consequences. If you publicly expose a large social graph of who pays whom, three things follow almost automatically:

· You make it easier to infer relationships and routines — roommates, partners, coworkers, habits.[3]

· You create a trail that can be cheaply mined by anyone from scammers to hobbyist bots.

· You create a tempting subpoena target for law enforcement and regulators.

Mozilla flagged the “public by default” model and noted that, at one point, “everyone on the Internet” could see your payments unless you changed the settings. Researchers have used Venmo data to map social and consumption networks at scale. Scams piggyback on the visibility of who frequently sends money to whom. None of that is a bug in the code. It’s the structural byproduct of a feed that treats economic behavior as social content.

Again: this is not the dystopian novel version of privacy loss. It’s the boring, incremental version — the kind that’s harder to dramatize and easier to live with until, in hindsight, it becomes the default for an entire generation.

The Upside Is Real — That’s Why It Won

If this were just a clumsy privacy failure, it wouldn’t have lasted. It worked.

Public feeds helped Venmo explode to tens of millions of users and hundreds of millions in revenue, riding network effects that traditional banks can only envy. It made splitting dinner painless, normalized P2P repayments, and, for many people, made “send me a check” sound like a joke.

From a coordination perspective, the trade-off is straightforward:

· Lower transaction friction and faster adoption.

· Higher exposure and more inference risk.

Most users never explicitly agreed to that exchange in a fully reflective sense. They just showed up, found their friends already there, and adapted. Path dependence did the rest, and visibility accelerated adoption in a way regulatory reputation never could have.

That’s why the “why is this public?” question is so revealing. By the time you ask it, the equilibrium the feature was designed to create is already there. Your confusion is a lagging indicator.

Visibility as the New Trust Technology

The banking world built trust by keeping your financial life out of sight and backing that promise with regulation and institutional capital. Venmo and similar platforms build trust by making your participation easy to see — to yourself, your friends, and, by default, more people than you probably realize.

In that sense, the public feed isn’t just a quirky social extra bolted onto a payment app. It’s the core of a different governance model for money:

· Trust shifts from institutional opacity to social observability.

· Privacy shifts from being an embedded property of the system to a user-level chore.

Venmo’s real innovation wasn’t giving us one more way to move dollars around. It was teaching us, very quietly, to treat our economic lives the way we treat everything else on a platform: as something meant to be seen.