The JetBlue – Spirit Fiasco and the Rise of Amtrak Economics

What happens when antitrust becomes stealth industrial policy: fewer low fare options, stronger incumbents, and a “public utility” airline no one voted for.

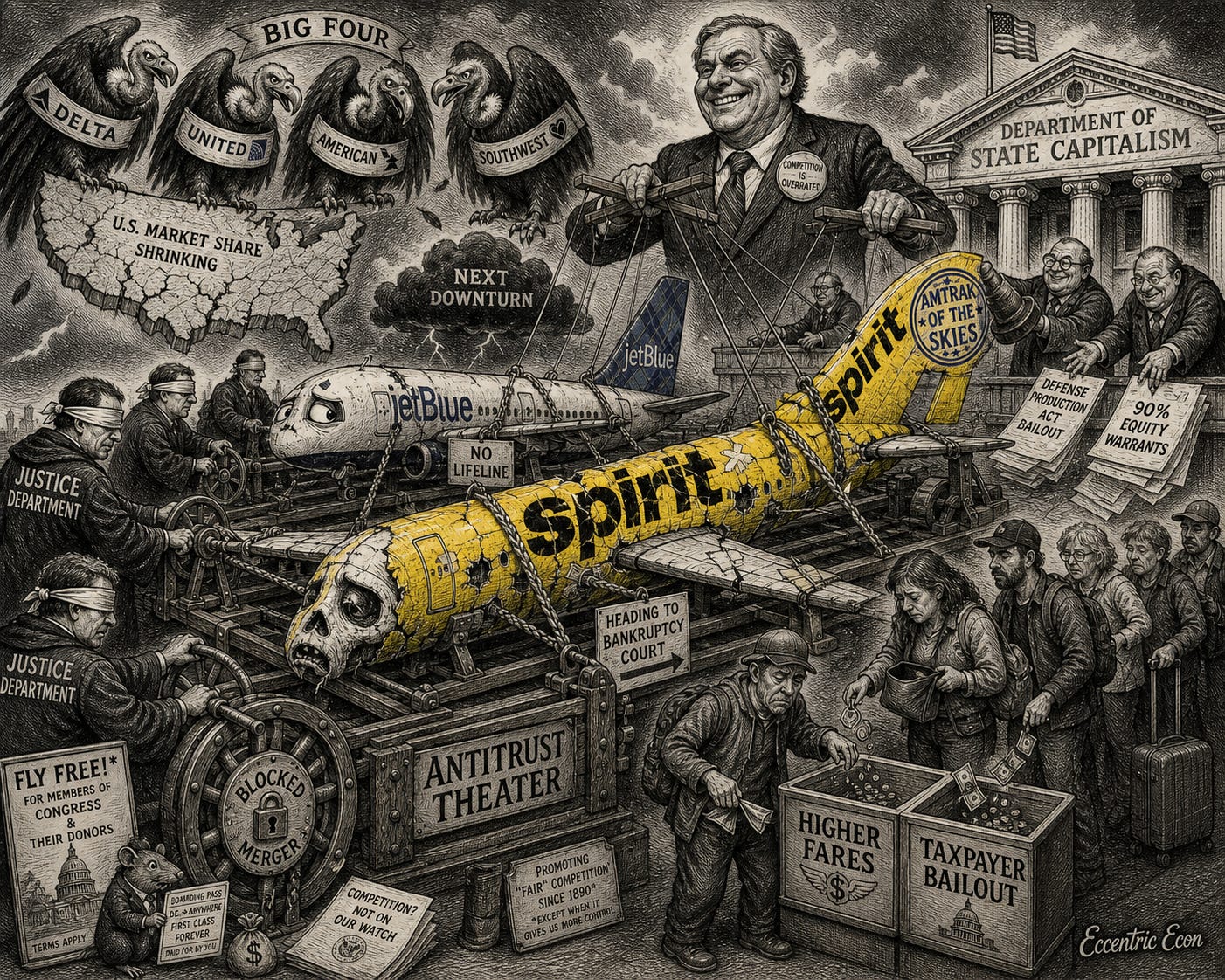

When the Justice Department went to court in 2023 to block the merger between JetBlue and Spirit Airlines, officials said they were protecting consumers from higher fares and less competition. It sounded like a victory for travelers, and US District Court Judge William Young certainly spun it as so in his January 2024 decision. A scant two years later, Spirit’s bankruptcy, JetBlue’s current struggles, and Washington’s flirtation with a federal bailout tell a very different story.

At the time, I argued that blocking the deal would not preserve competition so much as hasten Spirit’s collapse and leave JetBlue weaker, ultimately just strengthening the Big Four carriers that already dominate the market. That is exactly what has happened: Spirit has landed in Chapter 11, and JetBlue’s new CEO has been forced to publicly reassure investors that the airline will not file for bankruptcy this year, while pointedly leaving the prospects for 2027 unmentioned. The merger is dead, Spirit is in restructuring, and consumers are staring at the prospect of fewer flights at higher prices.

Now comes Act II. With Spirit in bankruptcy, the Trump administration is weighing whether to invoke the Defense Production Act to support a rescue package that could include up to $500 million in government-backed financing and warrants to purchase as much as 90 percent of the company once it emerges from Chapter 11. In other words, after the Biden administration’s blocking of a private merger on competition grounds, Washington is now toying with becoming Spirit’s de facto owner, which at least one clever analyst has dubbed an “Amtrak of the skies.”

The original sin: killing JetBlue - Spirit

Spirit was already in trouble when JetBlue proposed the acquisition, with mounting losses, heavy debt, and a business model that had been squeezed by higher fuel costs and intense competition. The merger offered a plausible path to keep its aircraft flying under a stronger, better-financed brand that could integrate Spirit’s planes and routes into a larger network. By blocking that path, DOJ did not freeze the industry in a healthy equilibrium; it simply forced the weakest player to try to survive on its own in a market dominated by giants.

Travelers across the country know what a concentrated airline market looks like. Four carriers already control roughly 70 percent of the U.S. domestic market, and at many major hubs, one airline reigns supreme. Ultra-low-cost carriers like Spirit and Frontier do not just offer cheap seats; they also provide leverage for price-sensitive travelers and a check on how far the big incumbents can push fares. When one of these discount options disappears, the legacy carriers gain bargaining power, whether or not they ever sought a merger.

The irony here is that antitrust officials claimed they were preventing JetBlue from becoming too big a rival to the legacy carriers. In reality, killing the deal simply cleared the way for the incumbents to tighten their grip on an already-captured market with no effort on their part, as Spirit shrinks and JetBlue fights for survival. Regulators protected a logo, not a viable competitor.

What an “Amtrak of the skies” really means

With talk in Washington of the federal government taking a direct stake in Spirit, we can draw an even more troubling conclusion. If private airlines cannot survive in a competitive market because regulators block the transactions that might rescue them, the emerging answer seems to be “don’t rethink the antitrust; embrace a new era of ‘state capitalism’ and take direct ownership instead.”

The structure being floated is not subtle. Reports describe a deal in which the U.S. would lend Spirit roughly $500 million, in exchange for warrants that could be exercised to acquire up to 90 percent of the equity if the airline exits bankruptcy. This is not a simple liquidity backstop; it is a path to effective nationalization – with a robust side quest of moral hazard – putting taxpayers on the hook for a chronically fragile carrier whose troubles were intensified by earlier policy choices.

Calling this “Amtrak of the skies” is not just a clever line. Amtrak’s history is a case study in what happens when the state takes over a struggling transportation system: routes that are hard to kill because they are politically popular, chronic operating losses, and perpetual pressure for more subsidies instead of true restructuring. State-backed airlines abroad, such as Alitalia in Italy, have shown similar patterns, cycling through rescues, political interference, and bankruptcy while governments supply bridge loans to keep the flag carrier alive. Once politicians become responsible for an airline’s fate, it becomes extremely hard to close unprofitable routes, renegotiate labor deals, or shrink capacity to a sustainable level.

In such an environment, the discipline of entry and exit – the very mechanism that is supposed to make markets work – is blunted or even eliminated. Routes are added or preserved to please members of Congress, Il Parlamento, or whatever government body is responsible for appropriations, rather than passengers; inefficient operations are funded with taxpayer money instead of being restructured or shut down. Consumers end up paying twice: first in taxes, then in higher fares from insulated incumbents who know they will be rescued if things go wrong.

Spirit’s potential bailout would be especially perverse because of the sequence. Regulators blocked a merger that might have preserved capacity under a stronger private carrier, then used the resulting collapse as justification for turning Spirit into a quasi-public utility. That these would be the actions of two different administrations is hardly an argument in favor, as it would simply reveal deep systemic issues that impact policy no matter who is in charge. Instead of a compromise between markets and planning, which rarely works in the first place, it is a way of locking in the costs of both.

The institutional mistake, not the market

The lesson of the JetBlue – Spirit debacle is not that airlines are too important to be left to the market. It is that antitrust authorities in Washington need more humility about their ability to micromanage complex, high fixed-cost industries from the comforts of D.C. conference rooms.

Airline economics are unforgiving: aircraft are expensive, fuel costs are volatile, and labor both organized and powerful. In that environment, blocking a merger because it might raise fares on certain routes, while ignoring the very real possibility of bankruptcy and exit, is a recipe for unintended consequences. A firm that cannot realistically survive the next downturn is not a durable competitive force, no matter how many economists who are willing to ignore the benefits of economies of scale you can find to testify about short-run price effects.

Future regulators should approach similar cases with a few simple principles:

Focus on viability, not just firm counts. A struggling carrier that is just one shock away from Chapter 11 is not the same thing as a healthy competitor, and keeping its brand alive at any cost is not the same thing as protecting competition.

Weigh dynamic effects. Ask not only “what happens to fares if we let this merger go through?” but also “what happens if we block it and the weaker firm fails anyway – and the government then feels compelled to nationalize the aftermath?”

Stop hiding industrial policy inside antitrust actions. If policymakers want to subsidize certain regions or routes, they should do so transparently by using straightforward tools, such as programs that pay airlines to serve small markets or voucher schemes that help travelers buy tickets, rather than blocking mergers and then turning failed firms into government-dominated carriers.

Right now, consumers are left with the bill. Spirit is in bankruptcy court; JetBlue is fighting to reassure investors and employees that it has a future. The Big Four carriers still dominate the skies, and passengers across the country face the prospect of fewer low-fare options than they might have had under a combined carrier. The Justice Department set out to protect competition; instead, they predictably made flying less competitive, more expensive, and opened the door to a potential new experiment in state ownership that will almost certainly make matters worse.

Like this kind of wonky autopsy on how Washington actually reshapes markets?

Subscribe to Eccentric Econ to get future pieces on antitrust, state capitalism, and institutional design delivered straight to your inbox.